By Jill Mehta

THE INTRODUCTION

The Non-performing Asset (NPA) problem in Indian Banks has been surging since a few years and no efforts, until Insolvency and Bankruptcy Code’s (IBC) launch, have helped to lessen the burden of NPAs on banks’ balance sheets. In February this year, the Reserve Bank Of India scrapped all the mechanisms like Credit Debt Restructuring (CDR), Structuring of Stressed Assets (S4A), Strategic Debt Restructuring (SDR) etc. which further urged banks to develop a better solution. No doubt, the IBC is active and is on the pathway to solve the problems, but it is still a new framework, which in turn means that it will take some time in settling down with a robust execution plan. Hence, arising out of this need was a proposal suggested by Sunil Mehta (Non-executive Chairman Of Punjab National Bank) Committee which will be an inter-bank framework to manage banks’ NPAs with a resolution plan developed by the consortium of Banks themselves.

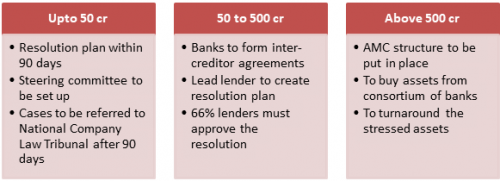

THE PROPOSAL

Here is how the committee proposes to segregate and deal with loans of varying levels:

THE PROCESS

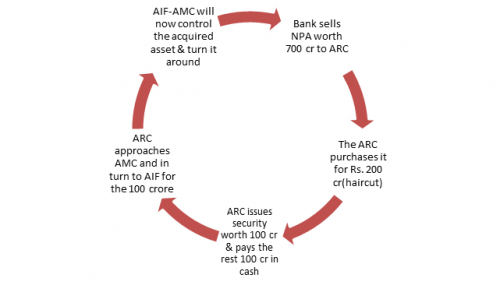

The Asset Management Company (AMC) has to redeem the security issued to banks within 60 days. The new AMC-Alternative Investment Fund (AIF) has to own at least 76% stake in the asset.

THE POSITIVES

Project Sashakt is a banker led initiative, hence the banks can mutually decide on the action plan to be undertaken for the NPA. Inter Creditor Agreement (ICA) will be ratified by The Board of Directors of the banks entering into the agreement which means banks are taking a conscious decision. It is a voluntary move rather than being a regulatory one like the Joint Lenders Forum (JLF).

The government is not going to interfere in the whole process, thereby leading to a solution that banks themselves are willing to accept.

THE CHALLENGES

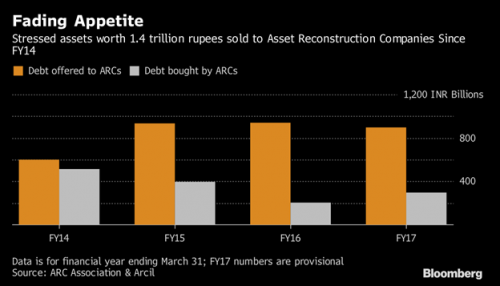

Lack of sufficient finances – The AMCs needs to raise money for the NPA’s which in itself is an obstacle given that there are not many takers for these stressed assets.

[Source: Bloomberg]

Deep Haircuts– The banks should be willing to take deep discounts for their NPAs in order for those to be sold.

Overlapping with IBC – RBI in its February circular said that all stressed assets worth more than 2000 crores if not resolved within 6 months should be taken to National Company Law Tribunal (NCLT). This accounts for about 70 big companies with loan amounting to Rs. 3.2 lakh crores. So Sashakt will essentially look into loans in SME sector with values less than 2000 crores.

Consensus on resolution plan– Some banks may have secured loan and others may have unsecured loan, therefore, to reach an agreement that takes into account the charges against the assets and to equalize the process for all banks remains a challenge.

Many banks have sold their assets to Asset Restructuring Companies (ARCs) so Inter Creditor Agreement should take into consideration the other institutes as well which own the NPAs.

Banks investing in AIF– No bank can contribute more than 10% in AIF and even so whatever amount has been contributed, the bank has to maintain a 150% capital charge.

49:51 – The deal is to get 51% of non-government ownership in AIF which is a huge challenge.

Pool of disbursed assets- Since NPA’s above 2000 crores are going to NCLT, the small loans which are spread over various banks might not be as attractive to the ARCs because they have to deal with a complex structure and less attractive amounts.

THE CONCLUSION

Project Sashakt, if well aligned to IBC, will clean up banks’ balance sheets. Though it is not a new framework in the first place – even earlier there have been efforts made to develop an AMC-ARC structure – the major difference this time is that the Inter creditor agreement is a stronger plan as compared to the earlier Joint Lenders forum (which was scrapped by RBI). Moreover, the time is ticking for NPAs that have stuck to the banks for so long. Essentially banks have only few options to resolve the whole mess –

1. IBC

2. Project Sashakt

3. Writing it off

Of course the better way would be to use the first two options rather than cutting down on their capital.

Disclaimer: The opinions expressed in this column are that of the writer. The facts and opinions expressed here do not reflect the views of IndusGuru Network Partners